SIPs are India's favourite investment habit — but the math behind rupee-cost averaging is misunderstood. Here's what it really does for your returns.

The SIP has become almost a religion among Indian investors, and for good reason. It's the simplest, most beginner-friendly way to start building wealth. But there's a lot of confusion about what an SIP actually does — and the marketing often oversells one specific benefit while underselling the one that matters most. Let's separate the myth from the math.

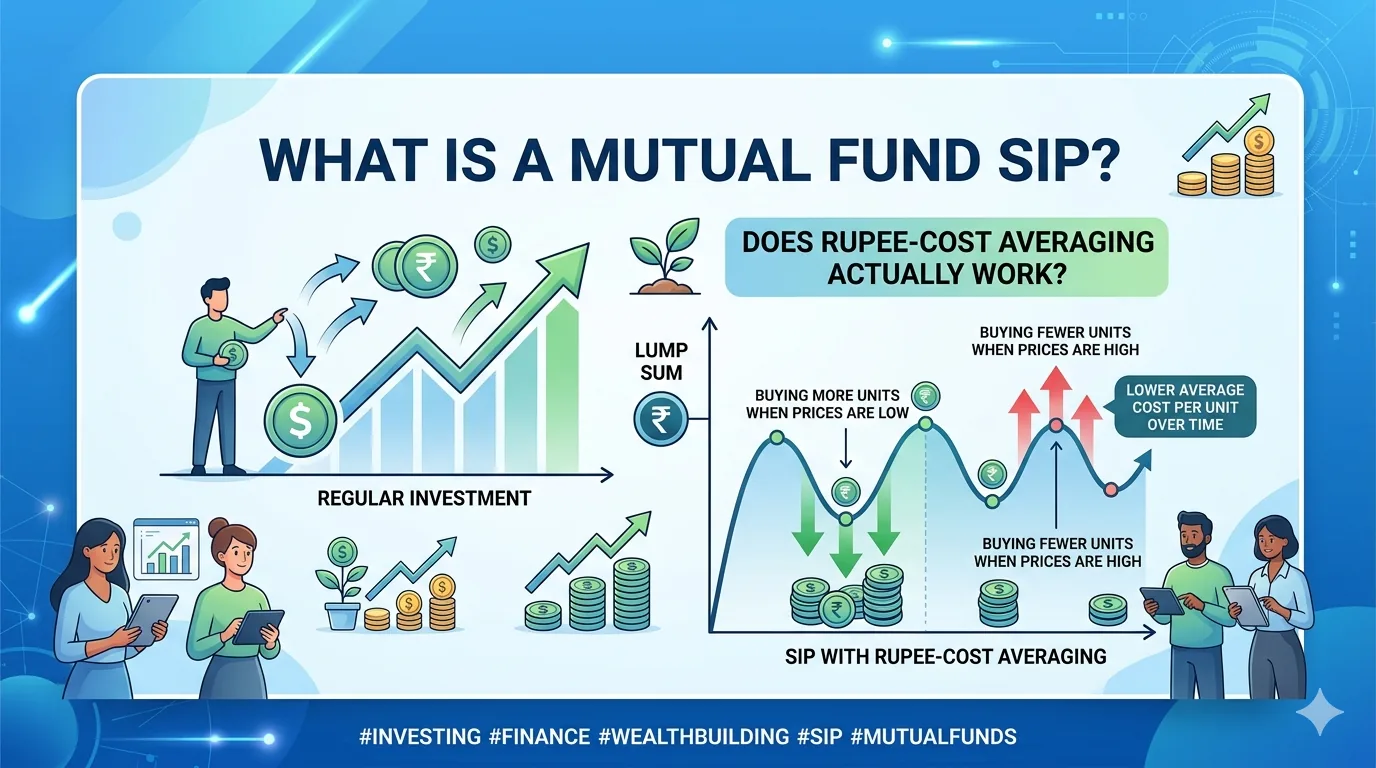

What an SIP actually is

SIP stands for Systematic Investment Plan. The idea is simple: instead of investing a large lump sum once, you invest a fixed amount — say ₹5,000 — automatically, at regular intervals, usually every month. The money is deducted from your bank account and used to buy units of a mutual fund, month after month, regardless of what the market is doing.

That last phrase is the whole point. Regardless of what the market is doing. You don't decide when to invest. You don't try to time the market. You just keep going, in good months and bad.

How rupee-cost averaging works

This automatic, fixed-amount investing produces an effect called rupee-cost averaging. Here's the mechanism, in plain terms.

Because you invest a fixed rupee amount each month rather than buying a fixed number of units, the number of units you get varies with the price. When the market is down and units are cheap, your ₹5,000 buys more units. When the market is up and units are expensive, your ₹5,000 buys fewer.

A quick illustration. Suppose you invest ₹6,000 over three months:

- Month 1: unit price ₹100 → you buy 60 units

- Month 2: market drops, price ₹60 → you buy 100 units

- Month 3: price ₹120 → you buy 50 units

You invested ₹6,000 total and got 210 units, an average cost of about ₹86 per unit — below the simple average of the three prices. The down month, which feels scary, is actually where the magic happens: your fixed amount scooped up the most units exactly when they were cheapest.

Over time, this smooths out your average purchase price and removes the impossible pressure of trying to buy at "the bottom."

What rupee-cost averaging does well

It removes timing stress. You never have to agonize over whether today is a good day to invest. The system handles it. This alone prevents countless bad decisions.

It turns volatility into a friend. For a long-term accumulator, market dips aren't disasters — they're discount sales where your SIP automatically buys more. This reframes the entire emotional experience of a falling market.

It builds discipline automatically. The hardest part of investing is doing it consistently, especially when markets are scary. An automated SIP makes consistency the default. You invest precisely when fear would otherwise stop you.

What it does NOT do (the honest part)

Here's where the marketing oversells. Rupee-cost averaging is a tool for managing behavior and risk — not a guarantee of higher returns.

In fact, there's a well-known nuance: if you happen to have a large sum available and the market mostly rises over your time horizon, investing it as a lump sum would often have produced higher returns than spreading it out, simply because more of your money was invested for longer. SIPs aren't mathematically superior to lump-sum investing in a rising market — they're superior at managing risk and psychology, which is usually more important for real human beings who don't have a lump sum lying around anyway.

So the honest framing is this: the greatest benefit of an SIP isn't a clever averaging trick. It's that it makes you a consistent, disciplined, unemotional investor — and consistency over decades, powered by compounding, is what actually builds wealth.

Common SIP myths to drop

- "SIP guarantees profit." No. An SIP is a method of investing in a fund; if the underlying fund or market does poorly over your horizon, you can still lose money. The SIP manages how you enter, not what you're entering.

- "I should stop my SIP when the market falls." This is exactly backwards and the single most damaging SIP mistake. Falling markets are when your SIP buys the most units. Stopping then defeats the entire purpose.

- "SIP only works for beginners." Even experienced investors use SIPs to invest steadily without the burden of timing.

- "More SIPs in more funds means more diversification." Spreading small amounts across a dozen similar funds just creates clutter, not real diversification.

The bottom line

An SIP is one of the best habits a new investor in India can build. Its real power isn't a magical averaging formula — it's that it removes timing stress, turns scary market dips into opportunities, and enforces the consistency that compounding rewards over decades.

Don't expect it to guarantee profits or beat every other strategy in every market. Expect it to do something more valuable: keep you invested, calm, and consistent through the cycles where most people panic and quit. That alone puts you ahead of the crowd.

Explore the verified SEBI RA's - https://kuberhunt.com/experts

This article is for educational and informational purposes only and does not constitute investment advice. Mutual fund investments are subject to market risks; read all scheme-related documents carefully. Past performance does not guarantee future returns. Consult a qualified, SEBI-registered professional before investing.