Assets, liabilities, debt, and the few numbers that actually matter. A beginner's guide to reading any company's balance sheet before you invest.

A balance sheet looks intimidating. Rows of figures, accounting jargon, totals that don't obviously mean anything. So most retail investors skip it entirely and buy a stock because someone said it would go up. That's exactly backwards. You don't need to be an accountant to learn what a balance sheet is telling you — you need to know which handful of numbers matter and what they reveal about whether a company is healthy or quietly drowning.

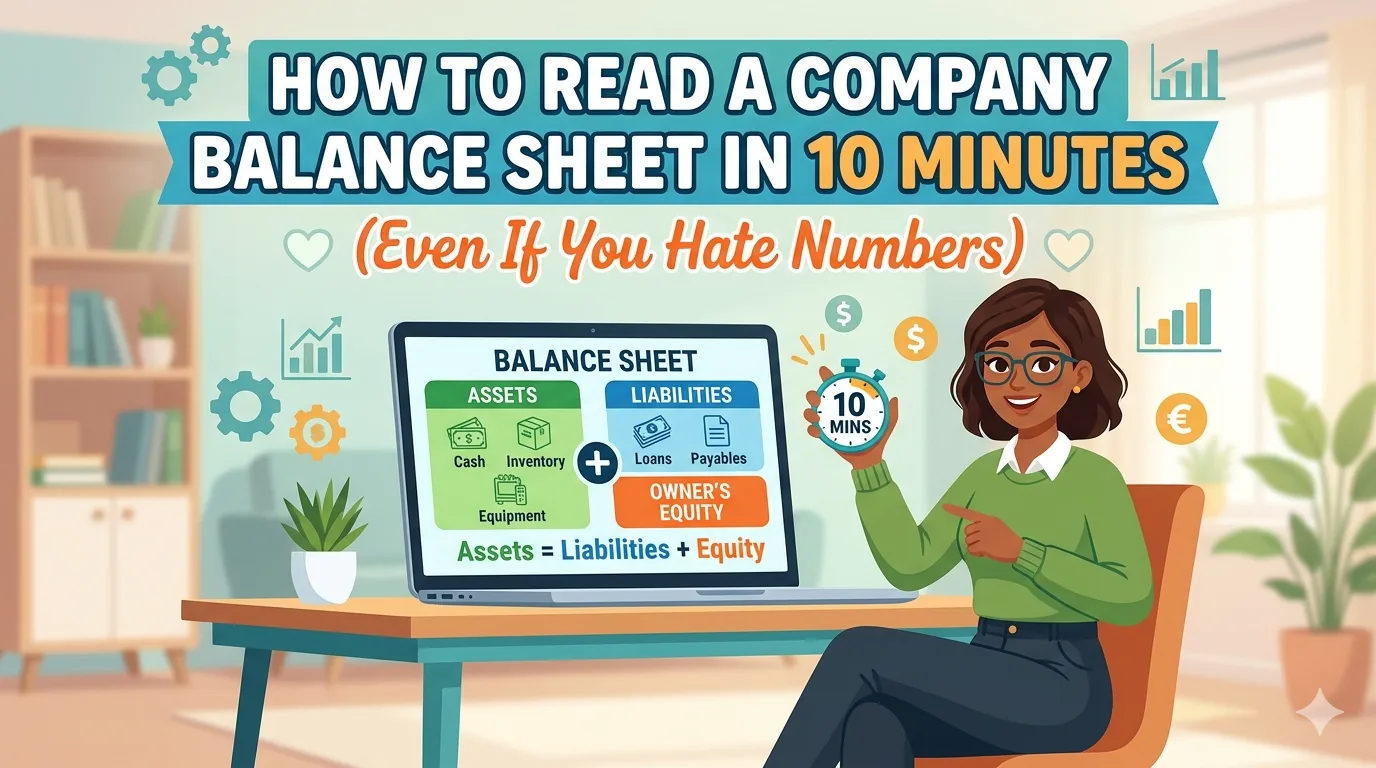

Here's how to do it in about ten minutes.

The one equation that explains the whole thing

A balance sheet is built on a single, almost childishly simple idea:

Assets = Liabilities + Equity

In plain English: everything a company owns (assets) was paid for either with borrowed money (liabilities) or with the owners' own money (equity). It "balances" because every rupee of stuff the company has came from somewhere. That's it. Once you see the balance sheet as "what they own, and who paid for it," the fear melts away.

The three sections you're reading

1. Assets — what the company owns. This splits into current assets (cash, money owed to them by customers, inventory — things expected to turn into cash within a year) and non-current assets (factories, machinery, long-term investments — the durable stuff). More cash and liquid assets generally means more flexibility and safety.

2. Liabilities — what the company owes. Also split into current liabilities (bills, short-term loans due within a year) and non-current liabilities (long-term debt). This is where you find the warning signs. A company swimming in debt is fragile, no matter how exciting its story.

3. Equity — what belongs to the owners. This is what would be left for shareholders if the company sold everything and paid off everything it owes. Growing equity over the years is a quiet sign of a business that's genuinely building value.

The numbers that actually matter

You don't read every line. You look for these:

Debt-to-Equity ratio. Take total debt and divide it by total equity. This tells you how much the company relies on borrowed money versus its own. A low ratio means the company is largely self-funded and resilient. A high ratio means it owes a lot relative to what it owns — risky if business slows or interest rates rise. What counts as "high" varies by industry (a bank or infrastructure firm naturally carries more debt than a software company), so always compare within the same sector.

Current ratio. Divide current assets by current liabilities. This answers a basic survival question: can the company pay its short-term bills? A ratio comfortably above 1 means yes, it has more coming in soon than going out soon. Below 1 is a flag worth investigating — it could mean a cash crunch is brewing.

Cash and cash equivalents. How much actual cash does the business sit on? Cash is oxygen. A company with healthy cash reserves can survive a bad year, invest in opportunities, and sleep at night. A company constantly scraping for cash is one shock away from trouble.

How to spot trouble in 10 minutes

Pull up three years of balance sheets side by side — most financial websites and the company's own investor pages provide them — and ask:

- Is debt rising fast year over year? Rising debt isn't always bad (a company might be investing to grow), but rising debt with no corresponding growth in revenue or profit is a serious red flag.

- Is cash shrinking? A steady decline in cash reserves while debt climbs is a classic sign of a business in distress.

- Is equity growing or eroding? Growing equity over time suggests a company building real value. Stagnant or shrinking equity deserves a hard look.

- Are receivables ballooning? If money owed to the company keeps growing faster than sales, it may be booking sales it's struggling to actually collect.

You're not trying to value the company to the rupee. You're trying to answer one question: is this a financially sound business or a fragile one? Ten minutes with these few numbers gets you most of the way there.

What a balance sheet won't tell you

Balance sheets are powerful but partial. They're a snapshot of a single moment, not a movie. They don't tell you whether the product is good, whether management is honest, whether the industry is growing, or whether the stock is cheap or expensive. For that you also need the income statement, the cash flow statement, and an understanding of the business itself. The balance sheet is the foundation, not the whole house.

The bottom line

You don't need an accounting degree to avoid the worst companies. Learn the single equation, understand the three sections, and check a few key ratios across a few years. That habit alone puts you ahead of the vast majority of retail investors who buy on tips and never glance at the financials.

A great business with a fortress balance sheet can survive almost anything. A weak business with a fragile one can collapse on the first bad quarter — no matter how good the story sounded.

Explore the verified SEBI RA's - https://kuberhunt.com/experts

This article is for educational and informational purposes only and does not constitute investment advice. Reading financial statements is one part of research and does not guarantee investment outcomes. Always do comprehensive due diligence and consult a qualified, SEBI-registered professional before investing.