STCG, LTCG, the ₹1.25 lakh exemption, and how your holding period changes your tax bill. A clear, no-jargon guide to equity taxation in India for FY 2025-26.

Nobody enjoys thinking about tax. But when it comes to your stock investments, a little understanding can save you a surprising amount of money — and more importantly, stop you from making expensive mistakes like selling one day too early. This is a plain-English walk through how capital gains tax on shares works in India right now, written for the ordinary investor, not the chartered accountant.

A quick but important note up front: tax rules change with every Union Budget, and your personal situation can affect how these rules apply. Treat this as education to make you a smarter, better-prepared investor — and confirm the specifics with a qualified tax professional before filing.

The one concept that controls everything: holding period

When you sell a stock for a profit, that profit is a "capital gain." How it's taxed depends almost entirely on how long you held the share before selling. This splits gains into two buckets:

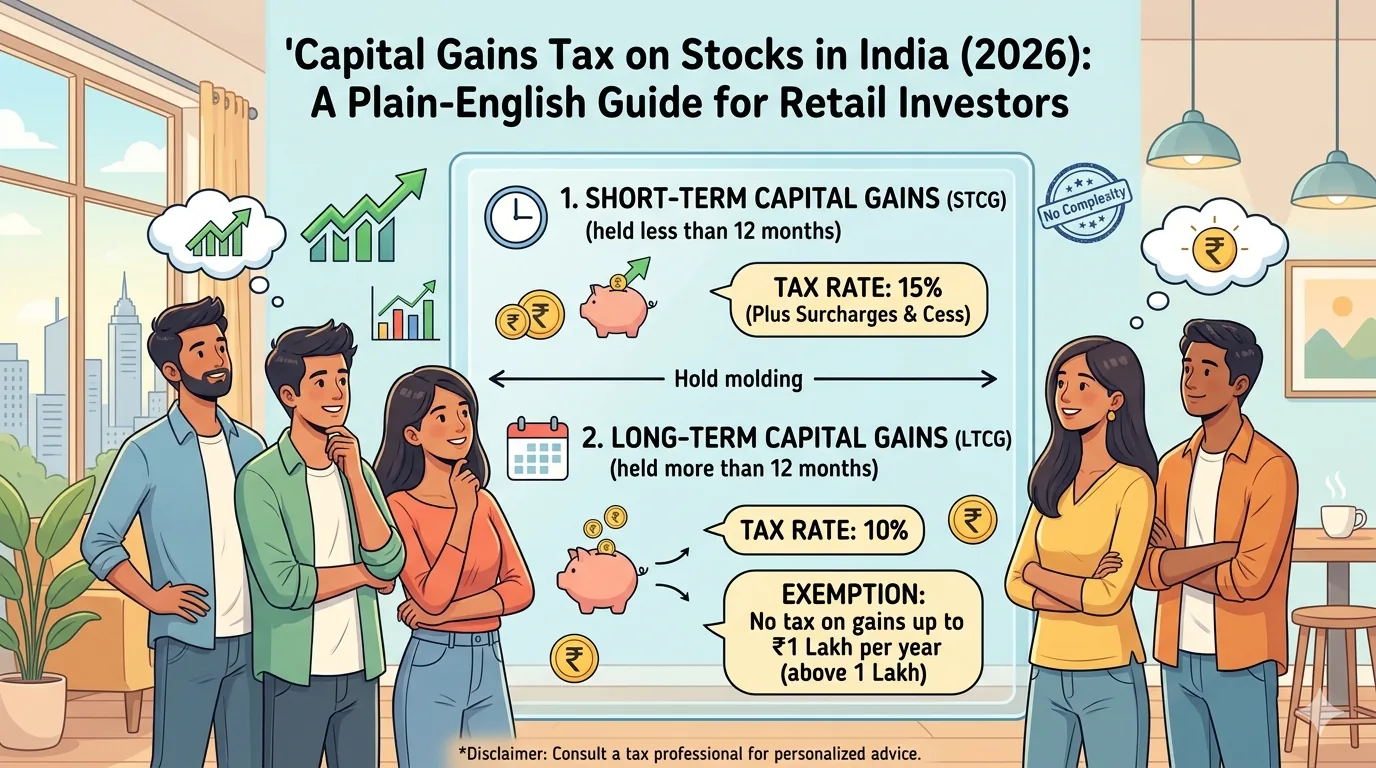

- Short-Term Capital Gain (STCG): You sold listed equity shares or equity mutual fund units within 12 months of buying.

- Long-Term Capital Gain (LTCG): You held for more than 12 months before selling.

That single dividing line — 12 months — changes your tax rate dramatically. Understanding it is the foundation of everything else.

The current rates (FY 2025-26)

These reflect the changes made in the Union Budget 2024, effective from 23 July 2024, which were left unchanged in the subsequent budgets:

Short-Term Capital Gains on equity: taxed at a flat 20%.

Long-Term Capital Gains on equity: taxed at 12.5%, but — and this is the part people miss — only on gains above ₹1.25 lakh in a financial year. The first ₹1.25 lakh of long-term gains each year is completely tax-free.

(All rates carry an additional health and education cess, and a surcharge can apply at higher income levels. This is where a tax professional earns their fee.)

Let that sink in, because it's the single most valuable thing in this article: an investor who sells after 12 months and one day pays 12.5%, with the first ₹1.25 lakh exempt. An investor who sells one day earlier pays 20% on every single rupee of profit. Same stock, same gain — wildly different tax bill, decided purely by patience.

A simple example

Say you buy shares for ₹4,00,000 and sell them for ₹5,50,000 — a profit of ₹1,50,000.

If you sell within 12 months (short-term): the entire ₹1,50,000 is taxed at 20% → ₹30,000 in tax (plus cess).

If you sell after 12 months (long-term): the first ₹1,25,000 is tax-free. Only the remaining ₹25,000 is taxed at 12.5% → ₹3,125 in tax (plus cess).

The difference is roughly ₹27,000 — for the cost of waiting. Now you see why the holding period matters so much.

Tax-loss harvesting: turning losers into a small win

Here's a technique most retail investors never use. If you have some investments sitting at a loss, you can sell them to "book" that loss and use it to offset your taxable gains — reducing your overall tax bill. This is called tax-loss harvesting.

There are rules about which losses can offset which gains. A useful one to know: short-term capital losses can be set off against both short-term and long-term gains, whereas long-term capital losses can generally only be set off against long-term gains. Used thoughtfully near the end of a financial year, this can meaningfully reduce what you owe — but get the mechanics confirmed with a professional, because the set-off and carry-forward rules have specifics.

The grandfathering clause (for long-time investors)

If you've held shares since before 31 January 2018, there's a valuable protection called the grandfathering clause. In simple terms, gains you accumulated up to that date are shielded — your cost of acquisition is adjusted to the share's fair market value as of 31 January 2018, so you aren't taxed on appreciation that happened before the LTCG regime came in. If you're a long-term holder, this is worth understanding properly, as it can significantly reduce your taxable gain.

Common mistakes to avoid

- Selling at 11 months out of impatience. You may be handing over 20% when a few more weeks would have dropped you to 12.5% with an exemption.

- Forgetting the ₹1.25 lakh exemption is per financial year. Some investors deliberately book long-term gains up to the exemption limit each year to use it rather than waste it. Worth a conversation with your CA.

- Ignoring losses. Letting a losing position sit without considering whether booking the loss could reduce your tax is leaving money on the table.

- Assuming rules are static. They aren't. What's true this year may change in the next Budget.

The bottom line

The Indian equity tax system rewards patience. Holding past the 12-month mark drops your rate and unlocks a generous annual exemption. Knowing the difference between short-term and long-term, using the ₹1.25 lakh exemption deliberately, and considering tax-loss harvesting are simple habits that keep more of your gains in your pocket.

But taxes should support your investment strategy, not drive it. Never hold a stock you should sell purely to dodge tax, and never make a tax decision on something this important without confirming it against the current rules with a qualified professional.

Explore the Verified SEBI RA's - https://kuberhunt.com/experts

This article is for educational and informational purposes only and does not constitute tax or investment advice. Tax laws change with each Union Budget and depend on your individual circumstances. Rates cited reflect FY 2025-26 rules at the time of writing. Always consult a qualified chartered accountant or tax professional before making decisions.