Walk into the world of paid financial advice in India and you'll meet three different professionals: the Research Analyst (RA), the Registered Investment Advisor (RIA), and the Mutual Fund Distributor

Walk into the world of paid financial advice in India and you'll meet three different professionals: the Research Analyst (RA), the Registered Investment Advisor (RIA), and the Mutual Fund Distributor (MFD).

All three are technically allowed to talk to you about your money. All three earn a fee. And almost nobody outside the industry can tell you, without Googling, what the actual difference is — or which one they should be paying.

Let's fix that. Because picking the wrong one costs you money in fees you didn't need or advice that doesn't match what you actually want.

The 30-second summary

Here's the cleanest way to remember the difference:

• A Research Analyst publishes recommendations to a group. One-to-many.

• An Investment Advisor gives personalised advice to you specifically. One-to-one.

• A Mutual Fund Distributor sells you mutual fund products and earns commission from the AMC. Not advice — distribution.

If you remember just that, you'll already be ahead of 90% of retail investors. But the details matter, because each one costs differently and serves a different need.

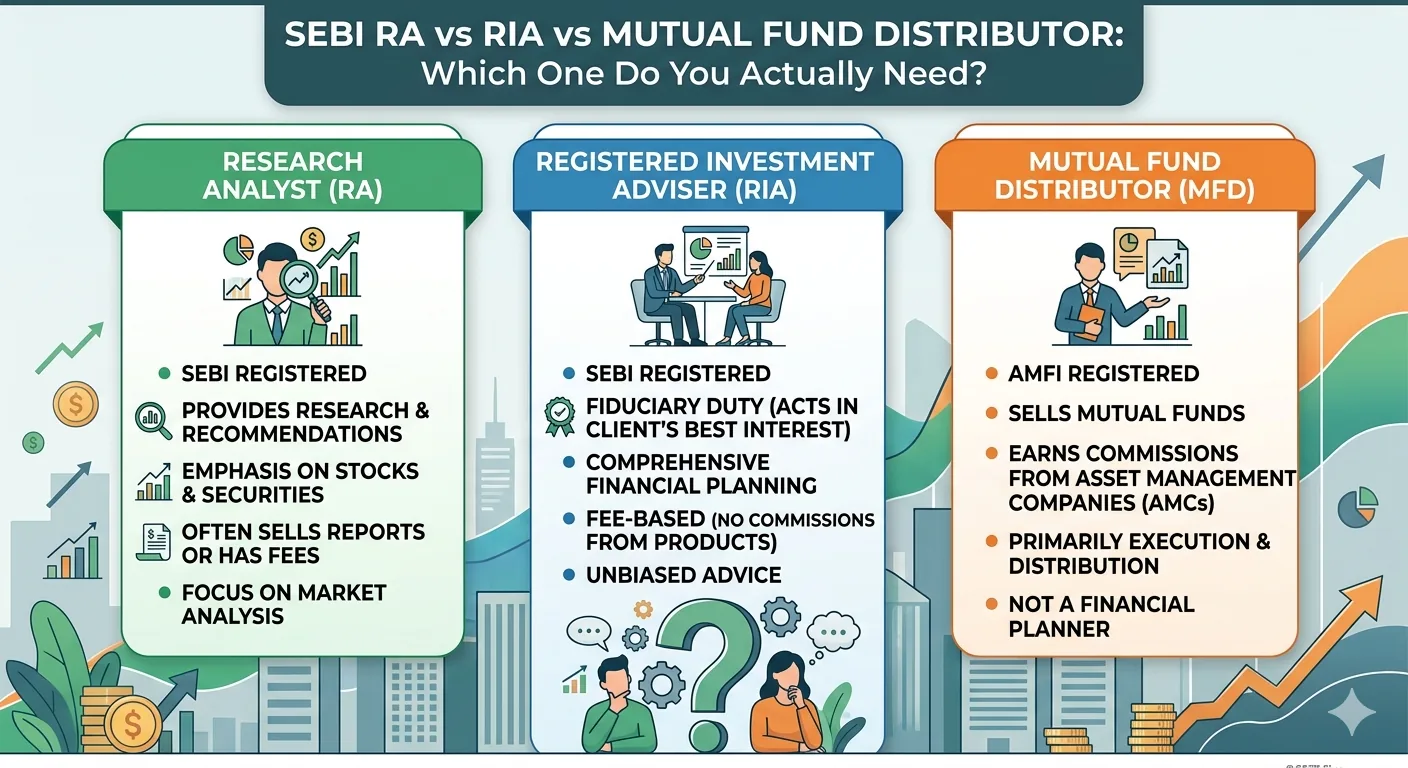

Research Analyst (RA): The publisher

Registration prefix: INH. Governed by the SEBI (Research Analysts) Regulations, 2014, with major amendments in December 2024.

An RA publishes research reports and recommendations that any of their subscribers can access. Think of them as a financial publisher: they put out a Modelfolio (a structured stock basket), a Reco Plan (specific buy/sell calls), or sector-focused research, and you subscribe.

Key features:

• Maximum fee: ₹1,51,000 per family per annum, across all SEBI-registered RAs combined.

• Cannot give you personalised advice tailored to your individual financial situation.

• Cannot guarantee returns.

• Must publish methodology, benchmarks, and validated performance for any model portfolio.

• Suited for: investors who want curated stock ideas without paying for a full one-on-one relationship.

Registered Investment Advisor (RIA): The personal advisor

Registration prefix: INA. Governed by SEBI (Investment Advisers) Regulations, 2013.

An RIA gives you personalised advice. They look at your full financial picture — income, goals, age, risk tolerance, dependents, existing portfolio — and recommend what you specifically should do. This is closer to the Western 'financial planner' model.

Key features:

• Two fee modes allowed: fixed fee (capped at ₹1,51,000 per family per year) or assets-under-advice fee (capped at 2.5% per year).

• Must execute a formal advisory agreement with you, including SEBI-mandated MITC (Most Important Terms & Conditions).

• Must follow strict suitability and KYC norms.

• Suited for: investors with complex situations — say, multiple income sources, retirement planning needs, family wealth, or first-time wealth creators who want a personal guide.

Mutual Fund Distributor (MFD): The seller

Registration prefix: ARN. Governed by AMFI (Association of Mutual Funds in India), not directly by SEBI as an advisor.

An MFD doesn't charge you a fee directly. They earn a commission (called 'trail commission') from the asset management company every time you invest in a mutual fund through them. Their incentive is to get you to invest, and to keep you invested, in MF schemes.

Key features:

• No upfront fee from you — but you're paying through the expense ratio of the regular plan you invest in (typically 0.5-1% per year more than direct plans).

• Cannot give 'advice' technically, but can recommend specific MF schemes.

• Cannot help you with non-mutual-fund products like direct stocks.

• Suited for: investors who only want to invest in mutual funds and prefer hand-holding through purchases, switches, and redemptions.

Side-by-side comparison

Feature RA RIA MFD

What they do Publish stock research Personalised advice Sell mutual funds

You pay Subscription fee Advisory fee Indirectly via expense ratio

Fee cap ₹1.51L/family/yr ₹1.51L or 2.5% AUA Not capped (commission-based)

Can advise on stocks? Yes (one-to-many) Yes (one-to-one) No

Can manage your account? No No No

SEBI prefix INH INA ARN (AMFI)

Best for DIY investors wanting ideas Holistic planning needs MF-only investors

Which one do you actually need?

If you're an active equity investor or trader who wants curated stock ideas: RA. You'll get Modelfolios, Reco Plans, or thematic baskets at a transparent fee. Most retail investors who're already comfortable picking and managing their own trades fit here.

If you're new to investing, have multiple goals (retirement + house + kids), and want someone to look at your full picture: RIA. The fee is higher because the work is deeper. But it pays back when you're making decisions like 'should I prepay home loan or invest the surplus?'

If you only invest in mutual funds and want a guide for SIPs and switches: MFD — but with eyes open. Direct mutual fund plans are cheaper. If you don't need the hand-holding, going direct saves you that 0.5-1% annual gap.

And remember: many retail investors do well with a combination — say, an MFD for SIPs and an RA for active trading ideas. The ₹1.51L fee cap is per RA category, not aggregate, so you have more room than you think.

Browse SEBI-registered Research Analysts on Kuberhunt → kuberhunt.com/experts

FAQs

Can the same person be both an RA and an RIA? Yes. SEBI's December 2024 amendments explicitly allow dual registration, provided the person maintains arm's-length segregation between research and advisory activities, and clients formally choose which service they're receiving.

Is a Mutual Fund Distributor cheaper than an RIA? Often it looks cheaper because there's no direct fee, but you pay through the higher expense ratio of regular plans. Over 10-15 years, that gap can exceed ₹2-3 lakh on a moderate portfolio. Cheaper isn't the right way to compare — it's about whether you need advice or just distribution.

Do I need an RIA if I already have an RA? Not necessarily. An RA covers your stock-research needs. You'd add an RIA only if you want personalised, one-on-one financial planning beyond stock picks — retirement, insurance, tax structuring, debt allocation.